Blended finance in South East Asia: Structural conditions for Australia’s financial system

Once the domain of governments, development banks and impact funds, more mainstream investors and banks are proactively participating in blended finance. For these financial institutions, blended finance is a win-win: allowing them to expand their investible universe and advance their sustainability goals through blended structures de-risked by government or philanthropic parties.

The Asia-Pacific is benefiting from this maturation of the blended finance market.

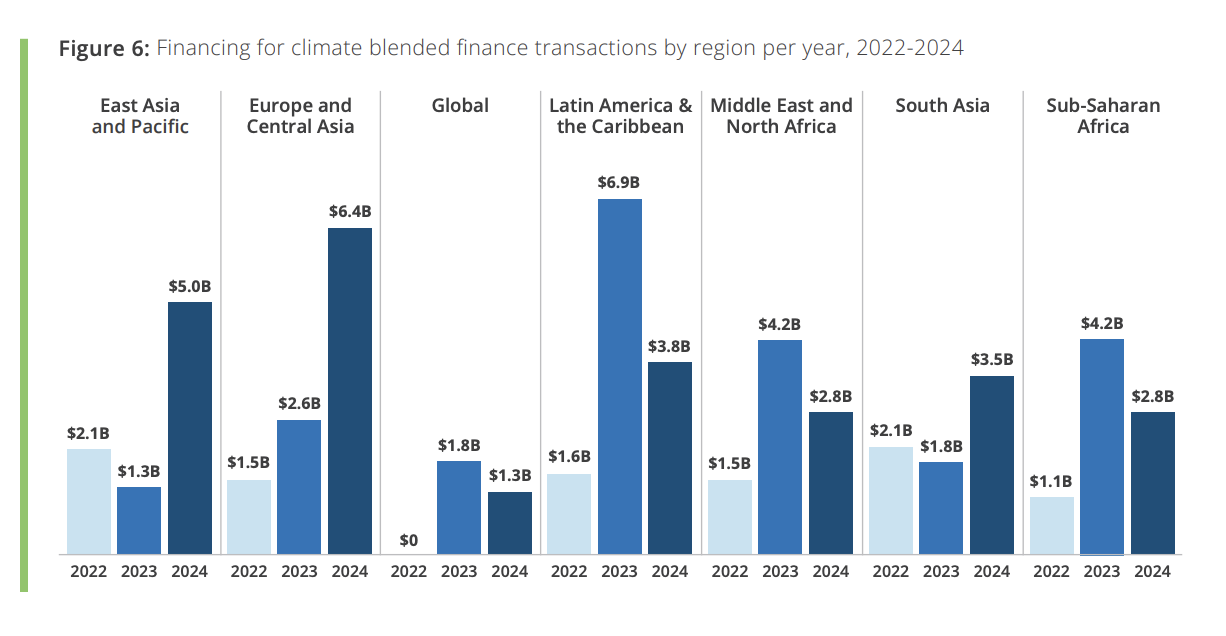

In East Asia and the Pacific, where the proportion of climate transactions increased by 77%[1] from 2023 to 2024, while Europe and Central Asia doubled over the same period. Southeast Asian countries which recorded a 10% increase in blended finance flows for climate in 2024.

As identified in Australia’s Southeast Asia Economic Strategy to 2040, Australian financial institutions are under-represented in Southeast Asia.

[1] State of Climate Blended Finance, 2025 p21

Could blended finance be a pathway for mobilising Australian capital into these fast-growing, geographically proximate, and strategically important markets?

With this question in mind, on Monday 8 December 2025, the Australian Sustainable Finance Institute (ASFI) and the Department of Foreign Affairs and Trade (DFAT) convened a working lunch in Sydney, hosted by Moody’s, bringing together Australian financial institutions and Joan Larrea, CEO of Convergence.

The discussion focused on what global experience is revealing about how blended finance markets are scaling, and what this means for Australia. Key findings are set out below, building on ASFI’s earlier analysis of how blended finance can unlock investment in Southeast Asia.

Blended finance is scaling globally, but Australian participation remains limited.

Blended finance combines concessional and commercial capital to improve risk-return profiles and crowd in private investment alongside developmental and climate outcomes. Globally, commercial banks, insurers, and asset managers are increasingly active in blended finance transactions, while Australian-headquartered institutions continue to play a limited role.

What is holding Australian institutions back?

Workshop participants identified a set of persistent execution barriers that continue to constrain Australian participation in blended finance, even as global momentum builds. Overcoming these barriers does not require reinventing the wheel but rather addressing the practical conditions that enable institutions to participate repeatedly, and at scale, in these transactions:

Scale and standardisation

Challenge: commercial financiers and investors can be reluctant to engage with structures that require lengthy development processes or repeated “first of a kind” effort, which add to the transaction costs and eat into returns.

Solution: Blended finance structures should be as close to ‘vanilla’ as possible, to keep transactions costs low (see Tamasek and HSBC’s Pentagreen fund). Securitisation of development bank loan portfolios (see Allianz’s SDG Loan Fund) and large concessional platforms (see UAE’s Alterra) are examples of how scale can be achieved.

Pathway to business growth

Challenge: For commercial actors focussed on client relationships, the value of blended finance for driving repeat business may be uncertain.

Solution: Clear signals about follow-on opportunities and the potential to establish relationships with partners that can provide repeat deal flow (such as MDBs and DFIs) would help to justify the upfront resourcing required to participate in blended finance.

Internal capability and incentives

Challenge: Blended finance requires specific expertise, including knowledge of and relationships with concessional capital providers. It may also require collaboration across multiple investment or lending teams, but silos within firms often means recognition can only accrue to one team, so the incentive to collaborate is limited.

Solution: Actors that engage regularly with blended finance typically establish dedicated blended finance teams with specialist expertise and the mandate to coordinate internal collaboration across deal teams.

Capital and regulatory settings

Challenge: For banks, capital bank weighting rules do not always reflect the downside protection that concessional capital provides, which means blended finance can appear less attractive on a balance sheet than the underlying risk profile suggests.

Solution: Commercial actors that engage in blended finance organisations typically have clear board or executive level direction. They also have organisational strategies that explicitly support blended finance, including recognition that these deals can take longer to execute and may require tailored treatment. While not a direct solution, clear organisational strategy and executive direction can help manage the issue.

Emerging momentum and the path ahead

There are early signs that the conditions for greater Australian participation in blended finance are beginning to shift. Globally, attention is moving toward scalable platforms and programmatic approaches, DFIs continue to play a market-making role in translating policy ambition into investable opportunities.

In Australia, recent regulatory and policy developments are also helping to reduce friction and support more coordinated action. In July, the Australian Competition and Consumer Commission granted formal authorisation for the co-design of blended finance structures, enabling ASFI to work with financial institutions and governments to collaboratively design new approaches where there is clear public benefit. This authorisation strengthens the ability of market participants to work together on complex structures, and supports collaboration aimed at turning climate, nature and social ambition into investment.

Government initiatives, including implementation of the Southeast Asia Economic Strategy to 2040, and targeted commitments such as investments via $2bn Southeast Asia Investment Financing Facility (SEAIIF), are helping build pipeline visibility and support deeper private sector engagement.

Australian investors are well-placed to deepen engagement in Southeast Asia through blended finance. However, scaling participation will require more than interest alone. Standardised structures, strategic alignment, stronger internal capability, and sustained public-private collaboration will be essential.

With demand for sustainable investment accelerating across the region, blended finance offers a pathway to unlock new commercial opportunities while delivering development impact.